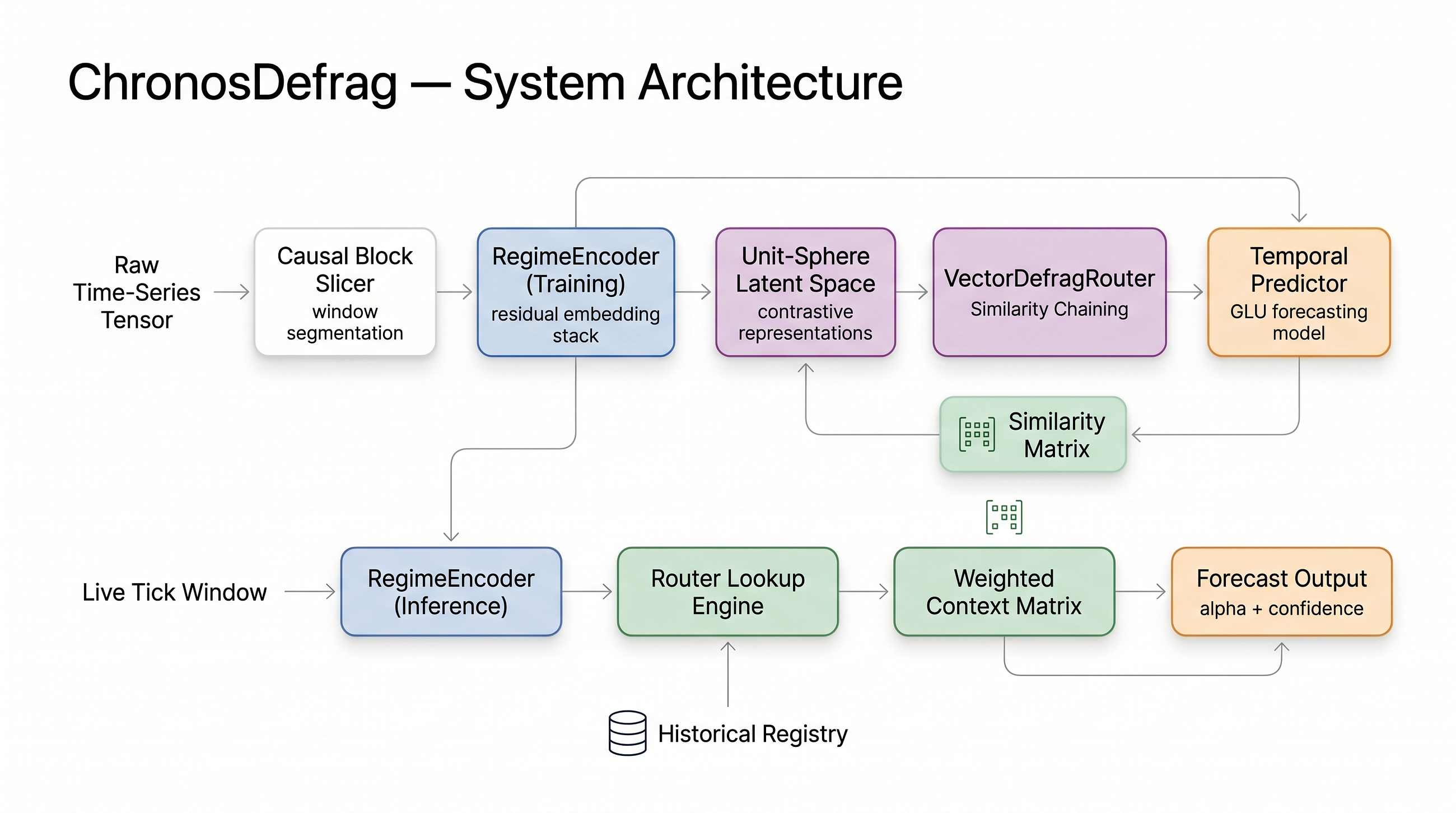

Standard deep sequence models applied to quantitative finance operate under an implicit assumption that is fundamentally broken…

Standard deep sequence models applied to quantitative finance operate under an implicit assumption that is fundamentally broken…Continue reading on Medium » Read More Python on Medium

#python